Backstory Post

2012

We did not pry ourselves out of our I-want-this-now-damn-it mindset for another few months. Just long enough to find ourselves signing another loan agreement.

WHAT?! ANOTHER LOAN!?!

Yes, let’s all pause and have a moment of silence to feel the shame soak in - you know, like on Game of Thrones….

Shame…

Tasman The Focus Kiwi rings a bell.

Shame…

Tasman The Focus Kiwi rings a bell

Shame…

One evening, Andrew took his scroll through Yachtworld (a website housing a huge number of sailboats for sale) and checked his email.

“Oh, a new email!” Andrew says. One of our friends are on the sailboat hunt for their own blue water cruiser. Unfortunately, the process has not been simple. This particular set of friends find a boat they think will work, pull it out of the water and have it surveyed only to find it’s not in good shape. Surveys are expensive, so each time they have to pull the boat out of the water, the cost meter ticks up another Boat Unit. What’s a Boat Unit? $1,000. Everything on a boat is measured in Boat Units.

Andrew grumbles his sympathies as he reads the latest update. “Maybe we need to get out there and see if our boat budget is realistic given the type of boats available? Yachtworld says its realistic, but I have no idea what the real condition of these boats are.”

“Sure, let’s get out there and check it out. It could be fun!”

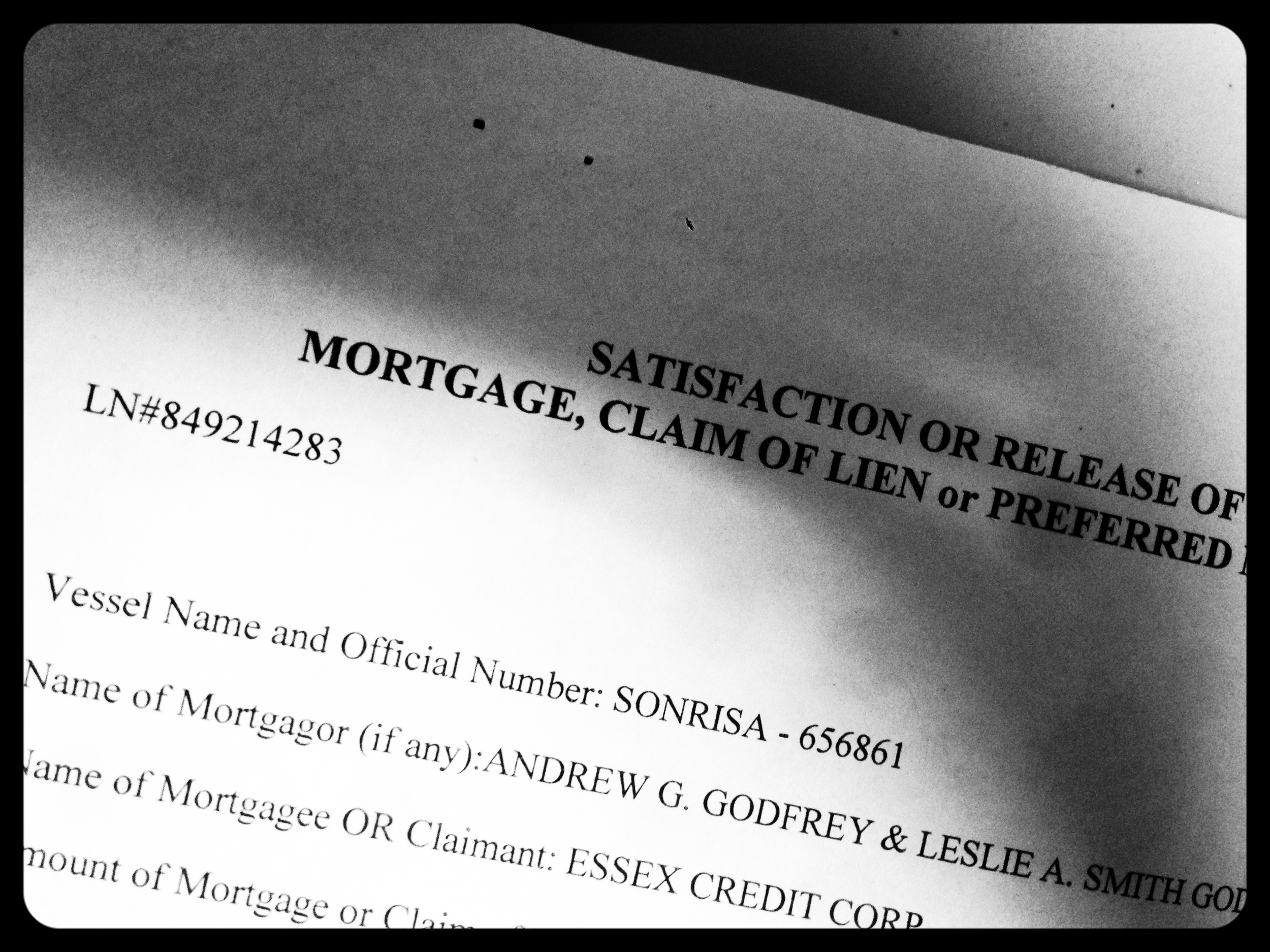

The next week, Andrew contacted a boat broker in San Diego, and we planned a mini-road trip to check things out. The trip went well. Too well, in fact. We didn’t just find that boats generally could fit our budget, we found the perfect boat that fit our budget. Sonrisa. www.oddgodfrey.com/oddlog/findingsonrisa1.

We returned home intent upon talking ourselves into abandoning reason, convictions, and common sense.

“Think about it,” Andrew said, “Trying to learn the boat, practice sailing, and complete the refit in one year while trying to work, too? Our one year plan is not reasonable. Three years in advance seems perfect.”

“Yeah,” I say, envisioning all the lovely weekends whale watching in temperate San Diego, “we need to test ourselves, get out to sea, sail more on the ocean.”

“Yeah,” Andrew says, “and the economy is so depressed right now, boat prices have to be lower than they otherwise would be. All the marinas have open spaces where wait lists use to be.”

“Yeah,” I say, envisioning myself swinging in a hammock on Sonrisa’s foredeck, “It’s like a home-loan anyway. Sonrisa will be our home.”

You can rationalize almost anything, and we did.

It was only after we were the proud owners of a blue water sailing yacht encumbered by a fifteen year boat loan at 8% that we dared to philosophically nose around in the mess we made with our spending spree. Had I nosed around earlier, I certainly wouldn’t have had in my possession a shiny new Honda, a fancy-pants top of the line new mountain bike, a beautiful piano I love to play, and the boat that will take me around the world.

So, what happened? Why did we abandon our hard won debt-free convictions? Did we regret it? What did we do next? What did we learn from this experience?

Let’s take the analysis one splurge at a time.

First, the car. Do I regret taking a 0% interest loan on the car? Yes. Why - 0%, that is free money!? By allowing me keep to the stockpile of cash we built up, the loan made the purchase of the car feel less painful - even though in reality there is a zero sum pile of money and that pile of money in my possession still must go to pay for the car. This little mental trick we played on ourselves caused us to buy a nicer (more expensive) car than we would have if we had to shell out actual green-backs. If I had to pony up my hard won cash up front, I probably would have second guessed the car, the type of car, the need for the car at all. Paying your own cash just feels different than using a loan.

Sonrisa. Do I regret taking a loan on Sonrisa? No. As it turned out, we really did need those three years to refit and learn to sail her. Having the extra year of experience was good, and I think we did sneak in and buy her in a good economic time for buying boats. But, our original convictions about debt remain. Debt is risk. Debt reduces freedom. Debt allows us to lie to ourselves about where our financial priorities really lie. We concluded we didn’t want to carry the loan any longer than necessary.

The mountain bikes and the piano. These were bought with cash, so the analysis here isn’t so much about the risk of debt but the tradeoff between living for today and saving for tomorrow. Do I regret buying the mountain bike and the piano? No. The last three years before we cast off were three of the most wonderful years of my life partially because of the experiences and joy Andrew and I gathered together using the mountain bike, the piano, and Sonrisa, too. But, there has to be a line. If we did everything that felt good today, we would never achieve what we want to achieve in the future. Building goals is necessarily a tradeoff between doing what feels good now in favor of what we want later. This balance is always tricky, and I'm not sure I have any good answers for how to analyze it wisely.

Knowing what I know now, I would tell my self of the past the following:

(1) Watch out for that moment when you reach debt payoff; the moment we thought we could relax is the moment we lost focus.

(2) You need to make a plan that includes a budget for fun today that won’t derail your goals for tomorrow. Had we planned to take a break between completing our debt payoff and beginning to pile up cash for the trip, we would have planned to buy the most sensible version of the things we need to experience joy today. We would have been less likely to go hog wild. We would have arrived at our sailing goal, and we could have stuck to our convictions better.

(3) Splurges happen. Time to pick up your shovel and dig yourself out again. Whenever you sell yourself out for some material object, you begin to carry a splurge-hangover. The quickest way I know to cure the pain of having splurged is to get back on track. Once the dust cleared, we immediately set to work to paying it all off again. We took the cash we had already stockpiled for the trip, ripped it away from ourselves and paid off the car loan. “Feel the pain, Leslie. Feel the pain of what you’ve done!” I told myself as I watched my cash clear out of my checking account and the loan disappear from the Honda website.

For the next year, every extra penny we had went to pay off Sonrisa. By November 2013, we were debt free again and ready to get back to the task of saving up our trip cash.